02

— New to Investing? —

Welcome to

Fierce Feminine Finance

For the woman who wants to turn savings into a freedom-based investment portfolio that quietly compounds her wealth while she eats croissants in Paris.

— Behind The Scenes —

Read about it on the blog...

How to Protect a Financial Windfall From Inflation, Taxes, and Expensive Mistakes

"If a lump sum is sitting in a standard savings account, inflation is quietly shrinking its purchasing power every single day."

You weren't expecting it. Maybe it came as a divorce settlement, a successful launch, an inheritance, or a bonus at work. Whatever the source, you suddenly have more money sitting in your account than you've ever had at one time—and instead of feeling excited, you feel a quiet, creeping panic:

What do I do with this? What if I mess it up? What if I make the wrong move?

First, take a breath.

The fact that you're asking those questions means you're already ahead of most women I meet.

Let me give you a clear framework for protecting and growing a windfall—covering three of the biggest threats to new wealth: inflation, taxes, and your own emotions. (That last one? Nobody talks about it enough.)

Why Listen to Me?

Hi, I’m Sarah Nicole Nadler, a financial coach and self-made millionaire who believes women deserve to feel powerful in every room their money enters.

Over the past decade, I’ve helped women:

• Turn six-figure inheritances into strategic portfolios

• Move from frozen to decisive

• Stop nodding politely in financial meetings they secretly don’t understand

I specialize in the space where strategy meets identity.

Because investing is not just math.

It’s about confidence. It’s about decision-making. And it’s about who you believe you are allowed to become.

I’ve worked with women who inherited six figures and felt paralyzed by the responsibility.

Women who had successful businesses yet froze when faced with choosing her first stock.

Women who hired advisors, nodded politely in meetings, and left feeling smaller than when they walked in.

Not because they weren’t intelligent.

But because no one had ever explained investing in a way that felt accessible, strategic, and aligned with how they think.

I’ve also seen the opposite transformation.

The moment a woman realizes she can understand asset allocation.

The moment she sees how fees compound over time.

The moment she recognizes that investing is following a framework—not a personality trait.

That shift changes everything.

My work blends practical investment education with emotional readiness, because money decisions made from fear look very different from those made from clarity.

And when you receive an extra $100,000—whether through savings, inheritance, settlement, or sale—clarity is the difference between empowerment and panic.

I am not anti–asset management companies.

They serve a purpose.

But I am deeply pro–informed decision.

Whether you decide to manage your investment portfolio yourself, or outsource it to an asset management company…

You deserve to know what your options are.

You deserve to know what you’re paying for.

And you deserve to know that managing investments is not reserved for a select few with special credentials or secret knowledge.

It is a skill.

And skills can be learned.

The information contained in this article is NOT financial advice. It's my strategy based on my own financial situation and experience, and is not the advice I would give to every client. If you'd like the support of a financial advisor to work out your own plan, click here to connect with my team.

The Real Threats to A Sudden Windfall

Threat #1: Inflation

Here's what nobody tells you when you receive a large sum: doing nothing with it is still a decision. If a lump sum is sitting in a standard savings account, inflation is quietly shrinking its purchasing power every single day.

That $200,000? In ten years, at a modest inflation rate, it may only buy what $160,000 buys today. You didn't spend a dime ...and you still lost.

This is why strategic deployment matters. Your money needs to be working, not just sitting.

Threat #2: Taxes

Depending on the source of your windfall, you may owe taxes on it—and the window for making smart decisions is narrow. Inherited assets, lawsuit settlements, divorce proceeds, and business sale profits all have different tax treatments.

Moving money into the wrong account type at the wrong time can cost you tens of thousands in unnecessary taxes.

This is where working with a fee-only CPA or financial strategist (not just any advisor, but one who actually understands your situation) becomes non-negotiable. [Looking for a place to start? My Accelerator program includes guidance on building your freedom-based investment portfolio without out-sourcing your power]

Threat #3: Emotional Decisions

This is the big one, and it's the one most financial content completely ignores.

All the financial plans and investment strategies in the world won't help a woman who is self-sabotaging her own wealth. And I say that with so much love... because I've been her.

When a windfall lands in your life, most women are still making decisions from the broke version of themselves. They haven't yet stepped into the version of themselves who knows how to handle that kind of money. And so decisions get made from fear, guilt, or excitement ...not from clarity.

That looks like:

Giving money to family out of guilt

Making a big investment without pausing to truly understand it (because it feels like you should be doing something)

Freezing and doing nothing for months while inflation quietly erodes it

Rush into a business deal or real estate investment because someone excited you about it

None of these are signs that you're bad with money. They're signs that you're human—and that you received a large sum without a framework for handling it.

The good news? You're about to have one.

So What Do You Actually Do With An Unexpected Lump Sum?

The honest answer? It depends on where you are in your financial journey.

I teach women a five-stage path called the Fear to Fierce Financial Formula™ and the right move with a windfall looks different depending on which stage you're in.

If you're still working through cash flow and budgeting basics (Overspend to Overflow™), this money needs a different home than it does for a woman who's already building her investment portfolio (Map HER Millions™) or optimizing her wealth for retirement (Retirement Runway™).

That said, there are three questions I get asked constantly when a woman comes into unexpected money—and they're worth addressing right now:

"Should I pay off all my debt first?" Hard no. Not all debt is created equal. High-interest consumer debt? Yes, tackle that. But using a windfall to wipe out a low-interest business loan or mortgage while leaving nothing invested is not a wealth-building move. I walk through exactly this in Credit to Capital™ (the stage inside my Map Her Millions Accelerator where we separate bad debt from smart leverage and use both strategically).

"How much can I spend on fun money?" You get fun money, always. My Cash Couture Formula™ is simple: pay your Wealthy Future Self first, then your Fun Money. Not fun money last, not no fun money. Just in the right order. You worked for this. You're allowed to enjoy it!

"What should I actually invest in?" That answer starts with you—specifically, the skills, experience, and ideas you've been overlooking as assets. My Million Dollar Magic Extraction™ process helps women uncover their own income-generating brilliance and start thinking about it as part of their portfolio (read my book From Hustler to InvestHER for more mindset tips in action). Once you know your magic, then we build the investment strategy around it.

With those questions answered, here's where a windfall can go to work.

The One Vehicle That Protects Your Windfall From Inflation, Taxes, AND Yourself

Here's the problem with receiving a large sum of money: the three biggest threats to it (inflation, taxes, and emotional spending) all start working against you the moment it hits your account.

Inflation is eroding it daily.

The IRS may already have a claim on part of it. And if it's just sitting there, accessible, the pressure to spend it (on family, on lifestyle, on the kitchen renovation you've been putting of) is relentless.

Most women lose a windfall not to one catastrophic decision, but to a hundred small ones made from guilt, fear, and the desperate need to just do something.

This is exactly the problem my OWL Method was designed to solve.

The OWL Method places your money into a specific wealth vehicle that does something most financial tools cannot do simultaneously: it grows your money, protects it from market losses, shields it from unnecessary taxation, and keeps it structurally out of reach from the emotional decisions that derail most women in the first 12 months after receiving a lump sum.

It also passes wealth to your beneficiaries cleanly, without the mess and cost of probate.

It is not a savings account.

This is not the stock market.

It isn't something most financial advisors will bring up in your first meeting, which is exactly why so many high-income women never hear about it until they're already working with me.

This isn't a replacement for your investment portfolio. It's the foundation underneath it. [Want to learn exactly how the OWL Method works? It's covered in full inside my Multiply Her Money membership.]

How To Choose What To Invest In

Managing your own portfolio is not day trading.

It’s not gambling.

And it’s not a skill anyone is "born with".

It is following a simple, repeatable sequence for making investing decisions quickly and with confidence.

This is where most women either freeze… or hand over control.

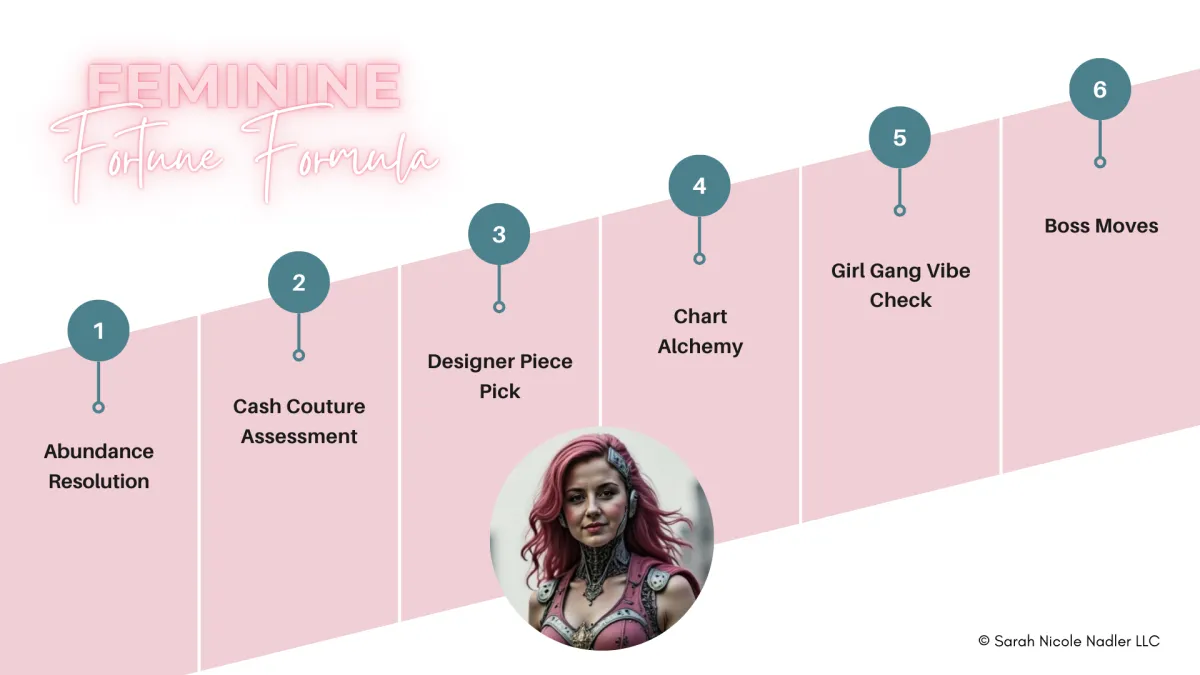

Instead, I teach what I call the Feminine Fortune Formula™—just six decisions in order so you never feel like you're guessing.

Here’s how it actually works:

✨ Step 1: Get Clear On Your Vision With My Abundance Resolution™

Before you move a dollar, we define why you’re investing.

→ Is this money meant to make you work-optional by 45?

→ To fund a luxury home purchase in 10 years?

→ To support your parents and pay cash for your daughter's wedding?

Clarity reduces fear. When you know what this money is meant to do, you stop feeling guilty for not having it “invested yet.” You move from pressure into purpose. That clarity alone removes 70% of anxiety.

✨ Step 2: Protect Your Based With A Cash Couture Assessment™

This is where we calculate your personal investing budget. How much stays liquid vs. how much goes to work?

→ Want to keep $20K available for “opportunities” and take $80K to build passive income? We map it.

→ Want to split your portfolio between a dream sabbatical in two years and retirement at 55? We do that, too.

You’ll never again wonder, “What if I need this money later?”

Because you’ll already know it’s covered.

✨ Step 3: Evaluate Investments With My Easy Designer Piece Pick™ Formula

My clients say this is their FAV part! I show you how to evaluate investments using simple criteria. If you can shop at Ross... you can master this ;-) because it's all about how we find designer-value investments at clearance prices.

→ If you’ve ever scored a pair of $700 heels for $130, you already get it.

→ We’re looking for undervalued gems—stocks, funds, or real estate deals—that are fundamentally strong and selling at a discount.

My AI-powered research tool does the heavy lifting.

You just need to know what you’re looking for—and this formula teaches you that, step-by-step.

✨ Step 4: Time The Market with Chart Alchemy™

Timing matters.

→ Think of it like catching a flight. If the flight is perfect but you arrive to the airport at the wrong time, you still miss the opportunity.

This step helps you avoid buying purely based on hype.

✨ Step 5: Confirm with Confidence And My Girl Gang Vibe Check™

Women are naturally collaborative decision-makers—but often we ask for opinions before we even know our own criteria.

In this step, I teach you how to check in with mentors, podcasts, articles, and peers without overriding your own power.

This is where you stop crowd-sourcing clarity.

✨ Step 6: Boss Moves™

Once your investment grows, you need new tax strategies, diversification and other boss moves to ensure you stay wealthy and continue to grow.

That's it.

Six structured decisions.

No guessing.

No gambling.

No handing over control out of fear.

When you follow a sequence like this, investing becomes strategic instead of emotional.

You log into your investing app and don’t panic.

You explain why you bought XYZ stock at brunch, and your friend asks you for advice.

You have a 10-minute convo with your accountant and don’t have to Google a thing afterward.

You open a statement and actually understand where your money went... and why.

You walk into an investor mixer and don’t feel like an imposter in heels.

That’s the difference.

You stop thinking: “Maybe I’m just not good with money.”

And start saying: “I know exactly why and how to make this next move.”

The Real Risk Isn’t Choosing Wrong

The real risk is:

• Freezing for 12 months while inflation eats purchasing power

• Outsourcing your power by handing your money to someone who will invest it in things you don’t fully understand

• Investing from fear instead of vision

$100,000 can change your future.

Or it can quietly leak in fees, hesitation, and avoidable mistakes.

The difference isn’t how smart you are.

It’s how much clarity you have.

Before You Move a Dollar…

So there you have it. It is absolutely possible to manage your own $100k+ investment portfolio. If you are sitting on $100K+ right now and feel the weight of getting it right…

✨ Your challenge this week: Schedule a call with my team for your free, no-obligation Map Her Millions Playbook before you make your next move.

On this call, we map out:

• Whether managing your own investments makes sense

• Whether outsourcing is strategically aligned

• What your next smartest step actually is

No pressure. No jargon. No intimidation.

Just clarity.

Because the real goal isn’t just growing your money. It’s becoming the woman who knows she could.

If this article helped you, DM me on Instagram (@sarahnicolenadler) and let me know your biggest takeaway!

Want to work with us?

The No-Fluff, No-Bro, No-Shame Wealth System for Well-Resourced Women Ready to Build, Manage, and Grow Their Own Million-Dollar Portfolio Without a Financial Advisor

COMPANY

CUSTOMER CARE

LEGAL

FOLLOW US

Copyright 2026. Sarah Nicole Nadler LLC. All Rights Reserved.